Corporate Tax Readiness Checklist (2025): What UAE Businesses Must Do

Corporate tax isn’t new anymore in the UAE, but 2025 is the year a lot of businesses get caught out. Not because the rules are impossible, but because small gaps, messy books, missing registrations, misunderstood free-zone benefits, unclear related-party transactions, stack up fast. And when they do, you’re looking at penalties, delayed filings, or an audit you didn’t budget for.

Most of these problems are preventable if you run the right checks early. That’s what this guide does. It walks you through a simple readiness checklist so you know exactly where you stand, whether you’re a mainland company, a free-zone entity trying to maintain QFZP status, or a business with cross-border transactions.

Corporate Tax Quick Facts

Under the Federal Tax Authority (FTA), the UAE implemented federal corporate tax through Federal Decree-Law No. 47 of 2022, effective from 1 June 2023.

- For 2025: taxable persons whose profits exceed AED 375,000 face tax at 9%; profits up to that may benefit from 0%.

- Large multinational enterprises (with global revenue of EUR 750 million or more) are expected to be subject to a 15% global minimum tax from 2025, in line with OECD Pillar Two rules once formally enacted by the UAE.

Registration with the FTA is mandatory for companies subject to tax. Failure to comply triggers administrative penalties.

If you have a mainland company or a business in a free zone, the rules differed, ad on

1. Financial Records & Bookkeeping

What clean books look like: Ledgers, trial balance, general journal entries for the year under review, reconciliations of bank, intercompany, fixed-assets, and inventory (if applicable). As per Federal Decree-Law No. 28 of 2022 on Tax Procedures, maintaining accounting records and commercial books is mandatory.

Timeline and roles: Start 3–6 months before your financial year-end. Your finance team or outsourced accounting services provider should reconcile and close books. Ensure depreciation, intercompany, and related-party entries are reviewed. Also, if you’re part of a tax group, note that under new ministerial guidance expected in 2025, audited financial statements will become mandatory for certain entities within tax groups. Businesses must prepare transfer-pricing documentation if they exceed FTA thresholds (AED 200 million turnover or AED 50 million in related-party transactions).

Red flags: Unreconciled intercompany balances, missing invoices, absence of fixed-asset register, foreign branch profits left unaccounted for, these signal weak bookkeeping and invite higher scrutiny.

2. Tax Registrations & Returns

Registration steps: If your mainland or free-zone company falls under taxable persons, register via the FTA’s EmaraTax portal. Late registration incurs an administrative penalty of AED 10,000. However, the FTA launched a waiver initiative: if you submit your first tax return (or annual declaration if exempt) within 7 months from the end of the first tax period, you may avoid the penalty.

Returns and linkage: File your corporate tax return within 9 months after year-end. The FTA urges compliance.

Responsible person: CFO or Tax Consultant needs to own the file. Deliverables: registration certificate, filing schedule, documentation mapping, and evidence of submission.

3. Transfer Pricing & Related-Party Transactions

What triggers review: Related-party transaction volumes, intra-group financing, offshore holdings, free-zone distribution activities. The FTA expects transparency and alignment with arm’s-length principles.

Actions: Document all intra-group transactions, invoices, service level agreements, financing terms. Engage Tax Consultants to prepare transfer-pricing documentation if your holding or trading business, or free-zone entity, transacts beyond de minimis thresholds.

Red flags: Missing policy, intercompany loans without documentation, services provided without charge or without contract. What this really means is you’re exposing yourself to audits or reassessments.

4. Payroll, Employee Benefits & Emirati Incentives (Including ICV Certification)

Payroll and benefits need to be aligned: Ensure that wages, stock options, commissions are properly reported for tax purposes and linked to your financial statements.

Incentives: If you operate in a free zone and rely on the qualifying free-zone person (QFZP) regime (0% rate), note that under Ministerial Decision No. 139 of 2023 (and related Cabinet Decision No. 100 of 2023), free-zone entities may qualify for the 0% corporate-tax rate on qualifying income if they meet substance and activity criteria.

ICV Certification: If your business engages in industries with inward-contract-value (ICV) certification (e.g., energy, oil & gas), ensure your contracts reflect ICV compliance and you retain certification evidence, since tax positions may reference “qualifying activities”.

Timeline: Review payroll and benefits documentation 3 months before year-end; evaluate if you are eligible for free zone exemptions or incentives and confirm ICV compliance where relevant.

Red flags: Untested free-zone eligibility, employee benefits not documented, missing ICV certificate or unsupported supplier contracts.

5. Compliance for Mainland Business Setup in UAE vs Business Set Up in UAE Free Zone

Mainland companies: Generally fully subject to corporate tax unless exempt under specific provisions. Check if your business is a “taxable person” under Federal Decree-Law No. 47 of 2022.

Free-zone entities: Can benefit from 0% rate if they meet substance, qualifying activity, and distributive rules via the QFZP regime.“Later ministerial updates in 2024–2025 have clarified eligible activities, substance requirements, and excluded income categories for the QFZP regime.

Checklist items: For free-zone entities, confirm your activity is listed as “qualifying”, verify transaction flow via free zone, meet substance test (local office, employees, decision-making in UAE). For mainland, ensure full compliance with registration and return filing.

Responsible roles: Company Secretarial advisor plus Tax Consultants.

Red flags: Free-zone entity doing non-qualifying trading without substance, mainland entity thinking it is exempt mistakenly.

6. When to Engage Tax Consultants, VAT Consultancy Services, CFO Services & Company Liquidation

Engage experts: If you’re unsure about registration applicability, transfer pricing, free zone eligibility, consider engaging Tax Consultants for a health-check. If you provide Accounting Services in-house, pair with an external CFO Services provider for oversight and strategy. VAT Consultancy Services are useful when your business handles both VAT and corporate tax.

Deliverables to expect: A “tax readiness report”, filing schedule with deadlines, compliance matrix, documentation index, risk map.

Company Liquidation: If you’re closing or liquidating your business, note that tax obligations don’t disappear automatically. Your liquidator and Tax Consultant must ensure final return submission, deregistration, and Records must be kept for at least 7 years from the end of the relevant tax period, per Federal Decree-Law No. 28 of 2022.

Timeline: Engage at least 6 months ahead of liquidation decision.

7. Common Penalties and Risks

Non-compliance brings real consequences. Under Cabinet Decision 75 / 2023, failing to register or keep records can trigger an AED 10,000 penalty per violation (AED 20,000 for repeat within 24 months) for violations such as incomplete records.

Late filing of corporate-tax returns can attract monthly administrative penalties that increase the longer non-compliance continues, as detailed in Cabinet Decision No. 75 of 2023.

Late payments accrue daily interest currently equivalent to roughly 14% per year, subject to FTA updates.

Audit triggers: mismatches between bookkeeping and returns, large inter-company flows, unclear free-zone eligibility.

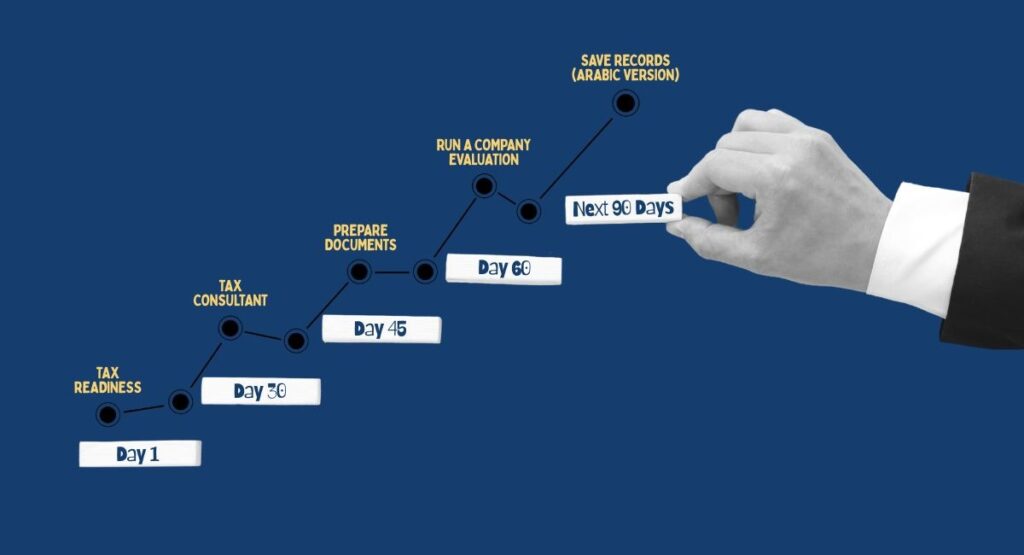

Practical Next Steps (Next 90 Days)

- Call your accountant or CFO-services provider: ask for a tax readiness review covering FY 2025.

- Engage a Tax Consultant or a VAT & TAX Consultancy Services firm: prepare a registration / return filing schedule, transfer-pricing documentation update, check free-zone status.

- Prepare documents: books closed, fixed-asset register, intercompany schedules, payroll & benefit summaries, ICV certificate (if applicable).

- Run a Company Evaluation: determine whether your entity qualifies for free-zone façade or needs restructuring.

- Save records: everything in Arabic version ready for inspection. Yes, the books must be auditable.

Quick Checklist

- Register for Corporate Tax via FTA (if applicable)

- Close and reconcile books: bank, assets, intercompany

- Document related-party transactions and transfer pricing

- Verify free-zone eligibility and substance (QFZP regime)

- Review payroll, benefits, ICV certification (if relevant)

- Engage Tax Consultant / CFO Services and prepare filing schedule

Disclaimer

This blog provides general information and does not constitute legal, tax, or financial advice. While all facts have been verified against official UAE sources (Federal Tax Authority, Ministry of Finance) and reputable accounting firms as of 2025, regulations and interpretations may change. Businesses should consult qualified Tax Consultants, accountants, or legal advisors before making decisions or taking action based on this content. The author and publisher are not responsible for any errors, omissions, or outcomes resulting from reliance on this material.

Sources:

U.AE

Reuters

وزارة المالية: الإمارات العربية المتحدة

وزارة المالية: الإمارات العربية المتحدة

Ministerial Decision No. 84 of 2025 on Audited Financial Statements for the Purposes of Federal Decree-Law No. 47 of

Deloitte

وزارة المالية: الإمارات العربية المت

وزارة المالية: الإمارات العربية المتحد

وزارة المالية: الإمارات العربية المتحدة

ms-ca.com

Chambers

Cabinet Decision No. (75) of 2023

FAQ

1. What is the UAE corporate tax readiness checklist for 2025?

The checklist includes:

- Financial Records & Bookkeeping: Ensure ledgers, trial balances, and reconciliations are accurate and complete.

- Tax Registrations & Returns: Register via the EmaraTax portal and file returns within nine months after your financial year-end.

- Transfer Pricing & Related-Party Transactions: Document all intra-group transactions and align with arm’s-length principles.

- Payroll, Employee Benefits & Emirati Incentives: Review payroll and benefits documentation; confirm ICV compliance where relevant.

- Compliance for Mainland vs. Free Zone Setup: Verify free-zone eligibility and substance; ensure mainland compliance.

- Engage Tax Consultants & CFO Services: Prepare a tax readiness report, filing schedule, and compliance matrix.

- Company Liquidation: Ensure final return submission, deregistration, and retention of records for at least 7 years under Tax Procedures Law.

2. When should a business start preparing for corporate tax in 2025?

It’s advisable to start preparations 3–6 months before your financial year-end. This timeline allows for thorough reconciliation, documentation, and compliance checks.

3. What documents are required for corporate tax readiness in UAE?

Key documents include:

- Financial Statements: Audited (if revenue exceeds AED 50 million) or unaudited but final and accurate.

- Tax Registration Certificate: Obtained via the EmaraTax portal.

- Transfer Pricing Documentation: Including invoices, service level agreements, and financing terms.

- Payroll & Benefits Records: Detailed and aligned with financial statements.

- ICV Certification: If applicable, ensure contracts reflect ICV compliance.

- Free Zone Eligibility Documents: Proof of qualifying activities and substance.

- Liquidation Records: If applicable, ensure final return submission and deregistration documents.

4. What is the deadline to register for UAE corporate tax in 2025?

Registration deadlines vary based on the date of license issuance:

- Entities incorporated before 1 March 2024: Registration deadlines are based on the license issuance date.

- Entities incorporated on or after 1 March 2024: Must register within three months from the date of incorporation. KPMG

For example, if your license was issued on 1 April 2024, the registration deadline would be 30 June 2024.

5. What penalties apply for failing to be ready for corporate tax in UAE?

Penalties include:

- Late Registration: AED 10,000 administrative penalty for late registration. alphapartners.co

- Late Filing: AED 500 per month for the first 12 months; AED 1,000 per month thereafter. FTA UAE

- Late Payment: Interest of approximately 14% per annum on outstanding tax amounts. FTA UAE

It’s crucial to adhere to deadlines to avoid these penalties.

6. How long does corporate tax registration take in UAE?

The registration process via the EmaraTax portal is typically straightforward:

- Preparation: Gather required documents.

- Submission: Complete the registration form and upload documents.

- Processing Time: Registration is usually processed within a few business days, provided all information is accurate and complete.

However, it’s advisable to initiate the process well before the deadline to account for any unforeseen delays.